This Ray Dalio piece on the problems and solutions for modern capitalism is an important piece of insight. It builds on his work on inequality and populism.

It is important as (1) he is a billionaire with considerable weight and clout

(2) it highlights the problems of both growing the (economic) pie and splitting the pie fairly

(Me: He omits natural/environmental capital in his primary analysis as a weakness)

(3) he observes social democratic/socialism ideas are better at (or at least focused on) pie splitting but free market type ideas have been better at (or at least focused on) pie growing

He pulls this together with a few other observations (amongst others) that

the left and right have never been further apart since the 1930s - they are entrenched and polarised

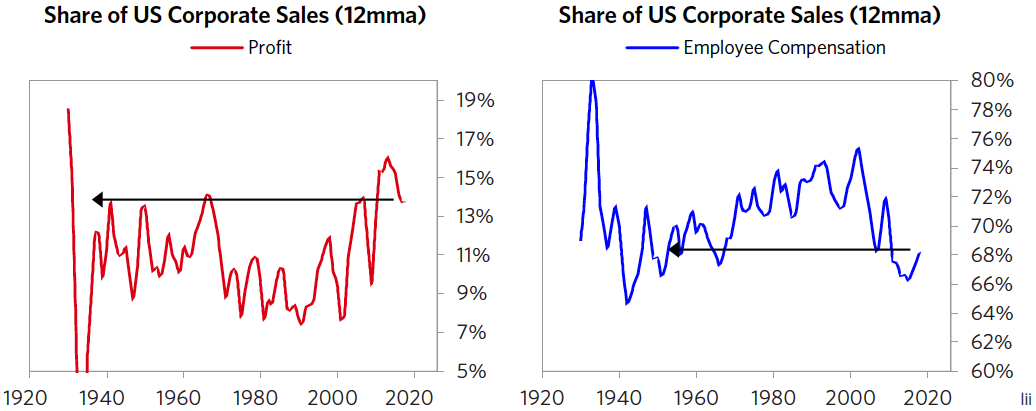

Technology (and other forces of capitalism) is continuing to disproportionately benefit the “haves”/rich ie owners of capital, automation will continue to displace workers

The US and China are at loggerheads with unknown outcomes

He has strong focus on the education inequality in the US amongst other insightful data (particularly on the bottom 60% and other data on the poor) and some insightful data on food poverty

(The childhood poverty rate in the US is now 17.5% and has not meaningfully improved for decades. In the US in 2017, around 17% of children lived in food-insecure homes where at least one family member was unable to acquire adequate food due to insufficient money or other resources.Unicef reports that the US is worse than average in the percent of children living in a food-insecure household (with the US faring worse than Poland, Greece, and Chile).

He then draws the important insight that it is systems problem:

“Contrary to what populists of the left and populists of the right are saying, these unacceptable outcomes aren’t due to either a) evil rich people doing bad things to poor people or b) lazy poor people and bureaucratic inefficiencies, as much as they are due to how the capitalist system is now working.”

He sketches out some solutions to work on including:

-i Leadership from the top

-ii Bipartisan working groups (ie left and right together)

-iii Co-ordination of fiscal and monetary policy together

-iv Clear metrics for success and accountability

-v Redistribution of resources that will improve both the well-beings and the productivities of the vast majority of people.

And within that a focus on good “double bottom line outcomes”

Ie outcomes that have good economic return and good social return

(for instance education fits that well)

(Again he misses out environment unfortunately, although many double bottom line ideas could be triple bottom line as well)

He proposes:

Create private-public partnerships (including governments, philanthropists, and companies) that would jointly vet and invest in double bottom line projects that would be judged on the basis of their social and economic performance results relative to clear metrics. That would both increase the funding for and the quality of projects because people who have to put their own money on the line would be responsible for them.

Raise money in ways that both improve conditions and improve the economy’s productivity by taking into consideration the all-in costs for the society (e.g., I’d tax pollution and various causes of bad health that have sizable economic costs for the society).

Raise more from the top via taxes that would be engineered to not have disruptive effects on productivity and that would be earmarked to help those in the middle and the bottom primarily in ways that also improve the economy’s overall level of productivity, so that the spending on these programs is largely paid for by the cost savings and income improvements that they create. Having said that, I also believe that the society has to establish minimum standards of healthcare and education that are provided to those who are unable to take care of themselves.

While you can argue about the diagnosis and cause of the problem, the data is insightful, and the solutions are food for thought.

Unfortunately, I am fairly pessimistic about most of those solutions given what I can see about the politics of the UK and US (and others) although some countries may fare better (eg New Zealand which I feel is working on i and iv)

But there are elements of v. I can see working although this may only come through if our leaders can take a longer view and whole-view lens (for instance, increasing educational and social resources in areas of poverty brings long term returns but is short term costly and painful; carbon taxes are hard to fall progressively on society)).

And in theory there’s no reason why i - iv couldn’t happen but it would take a moment or time of social cohesion and cultural change to get there. We don’t have that. But it could happen as I talk about in my performance-lecture Thinking Bigly.

Full Essay by Dalio here:

https://www.economicprinciples.org/Why-and-How-Capitalism-Needs-To-Be-Reformed/

A blog on his populism work:

https://www.thendobetter.com/investing/2019/1/5/ray-dalio-on-cycles-populism-trade-wars