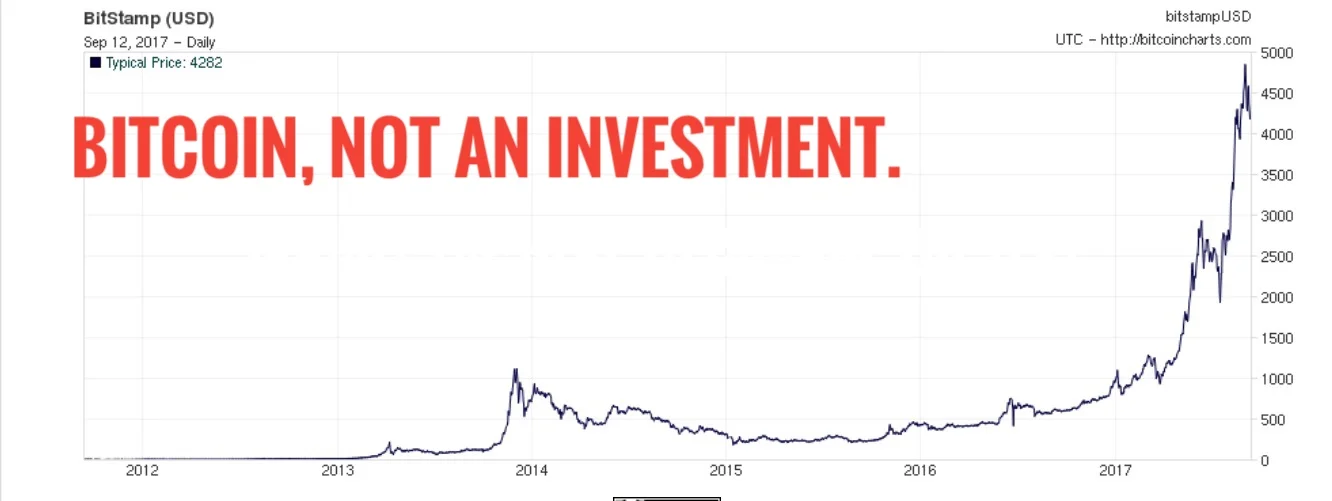

Bitcoin is not an investment (as I define it). It is a money or a currency. You can speculate in it and trade in it. But I do not think it has a major place for most people as an investment, just like most people would not have South African Rand as an investment.

It does reveal facets of modern money, which we often ignore. Money relies on belief. Money relies on trust. Its value relies on a network of people who accept it as money. It helps that you can exchange if for goods, services and other currencies. It is not backed by gold, goods or tax.

Go back in time. Sea shells were used as money.

The traditional qualities of money: durability, handiness or convenience, recognizability and divisibility were mostly embedded in shells. (Large shells and small shells harder to divide but easier than camels). Cowry shells were still used as currency until the 20th century.

Fiduciary (or trust, fiat) currency was used in China over 2000 years ago, so in that respect bitcoin has a distinguished history to draw upon.

Howard Marks in his latest September memo (here are some thoughts on his July memo) partially adjusts his view on bitcoin, also concluding it is money, but sharing my view (or perhaps I should be sharing his view, Marks being much more distinguished than me!) that is it not a good investment. If you fancy a gamble, sure why not? But know it for what it is. A speculation. Perhaps like gold, it could have a place as geopolitical hedge, as money/gold has done over history, but I still don’t think that makes it an investment. It could make it a “safe asset” (see Andolffi below) but again I’m unsure that’s an investment.

Bitcoin could possibly be valued. There are some valiant attempts. The assumptions and data needed do seem to put it in the realm of speculation. But, if interested look at some of these writers below:

David Andolfatto (who works for fed reserve bank of st louis) is great on bitcoin - blog here . His view seems to be bitcoin is lousy money but a possible store of value. This slide deck here gives a thorough overview of Bitcoin that I recommend.

Tony Yates (former Bank of England) talks about the barriers to cryptocurrencies taking over at an FT guest post.

If you'd like to feel inspired by life lessons try: Ursula K Le Guin on literature as an operating manual for life; Neil Gaiman on making wonderful, fabulous, brilliant mistakes; or Nassim Taleb's commencement address; or JK Rowling on the benefits of failure. Or Charlie Munger on always inverting.

Eric Lonnergan on an overview of Bitcoin’s characteristics including “intelligence” in aspects of “self-regulation” (I’m personally unsure if that’s ‘true’ intelligence cf. Shells, gold) . Lonnergan writes: “Bitcoin’s ‘intelligence’ involves the application of a very simple rule: the quantity expands to 21 million and then it ‘grows’ at zero percent. I’m less interested in the merits of this rule, which are well-rehearsed, than the possibilities it suggests. The ‘intelligence’ of money could be extended in many interesting ways. From an economic standpoint, the obvious improvement in intelligence would be to design a currency which expands and contracts in line with demand for currency. Embedding this in the currency’s DNA would render central bank decision-making redundant – to everyone’s advantage. ‘Intelligence’ could also embed social goals – for example the currency could self-regulate the activities for which it is used, perhaps even rewarding or punishing activities contingent on their social impact.”

Howard Marks is always worth reading if you have any interest in markets and the world.

Marks caution joins the chimes of Ray Dalio (post here), John Hussman (post here) along with Albert Edwards (currently at SocGen (with Andrew Lapthorne, his recent chart here), and to some extent James Montier (who also worked alongside Albert at DK previously, but has a behavioural economist streak to his work; now at GMO) and Jeremy Grantham (at GMO) have tended to put quite some weight on these type of metrics and valuation discipline, at least for long cycle returns (around 7 years). It's interesting that most of this group are chiming quite loudly, with the possible exception of Grantham who is ringing in a slightly different key (suggesting much slower reversions to the mean than before).

The world of macro has so many cross currents.

There is another interesting chime with Nassim Taleb's thinking from his pop risk books. This idea that we do not handle "fat tails" or "Black Swan" events very well. That models do not account for these events well (real world is not "normal" or "gaussian"). This dovetails well with Hyman Minsky's observation/theory on why we have and will always have boom/bust cycles.